Once you have established your Dental Professional Corporation (DPC) and your practice is generating revenue, the next major financial decision is determining how to extract that money for your personal use. The Canada Revenue Agency (CRA) generally provides two primary methods for business owners to pay themselves: salary or dividends.

At Capstone LLP, we work closely with dental professionals to design highly tax-efficient remuneration strategies. In this post, we explore how dentists should approach paying themselves from their DPC, the impact of corporate investment income, and a very costly tax trap that recent graduates must avoid.

How Dentists Should Pay Themselves from a DPC

There is no one-size-fits-all answer to the “salary versus dividend” debate; the optimal choice depends entirely on your personal financial goals, your corporate structure, and your stage in life.

The Case for Salary

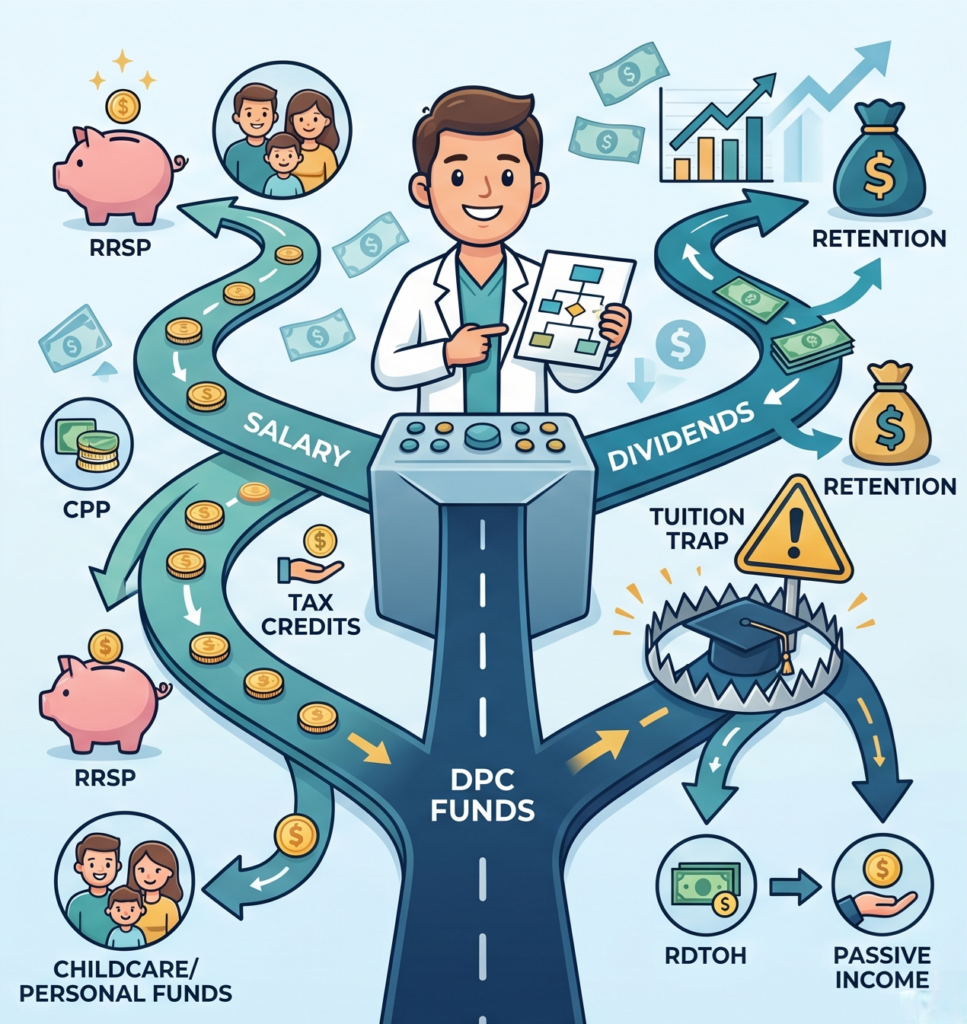

When you pay yourself a salary, the corporation deducts the gross wage as a business expense, and you pay personal income tax on the earnings.

- RRSP Contribution Room: Salary is considered “earned income,” meaning it generates Registered Retirement Savings Plan (RRSP) contribution room for the following year.

- CPP Contributions: A salary requires you to pay into the Canada Pension Plan (CPP). While this involves both employee and employer matching contributions, it ensures you are building a guaranteed, inflation-indexed pension for retirement.

- Child Care Expenses: If you have children and incur daycare expenses, claiming the child care expense deduction on your personal tax return requires earned income (salary).

The Case for Dividends

Dividends are paid out of the corporation’s after-tax retained earnings. Because the corporation has already paid tax on this money, you receive a Dividend Tax Credit personally to prevent double taxation.

- Simplicity: Dividends do not require payroll registration, monthly source deductions, or CPP remittances. You simply declare the dividend and issue a T5 slip at the end of the year.

- Cash Flow: Without CPP premiums, paying a dividend can sometimes leave slightly more immediate cash in your pocket, though this comes at the cost of giving up future CPP benefits and RRSP room.

The Role of Passive Income and RDTOH

As your DPC matures, you will likely begin investing surplus cash inside the corporation (such as in stocks, bonds, or real estate). Under Canadian tax law, passive investment income earned inside a private corporation is subject to a high upfront tax rate (nearly 50% in Ontario).

However, a significant portion of this tax is refundable to the corporation. It is tracked in a notional account called Refundable Dividend Tax on Hand (RDTOH).

To trigger a refund from the RDTOH account, the corporation must pay out taxable dividends to its shareholders. Specifically, for every $1 of taxable dividends paid out, the corporation recovers $0.38 from its RDTOH account. Therefore, if your DPC holds a robust portfolio generating passive income, incorporating some level of dividend into your remuneration strategy generally makes absolute tax sense. Failing to pay a dividend in this scenario means leaving the corporation’s refundable tax dollars stranded with the CRA.

The Tuition Credit Trap: A Warning for Recent Graduates

While a mix of salary and dividends is ideal for established dentists, recent dental graduates face a highly specific—and very costly—tax trap.

Dental school generates massive tuition tax credits. If you have a significant carryforward balance of unused tuition credits, paying yourself exclusively via dividends from your new DPC can lead to disastrous tax consequences.

How the Trap Works

Both tuition credits and the Dividend Tax Credit (DTC) are non-refundable tax credits. However, Section 118.92 of the Income Tax Act dictates a strict, mandatory order in which personal tax credits must be applied on your tax return:

- When you receive a dividend, it triggers the Dividend Tax Credit, designed to prevent double taxation.

- However, the CRA forces you to apply your carryforward tuition credits to bring your basic federal tax payable down to zero before the Dividend Tax Credit can be applied.

- Because your tuition credits wipe out the tax liability first, the Dividend Tax Credit has nothing left to offset. Because the DTC cannot be carried forward to future years, it is permanently wasted.

By paying a dividend in this scenario, you are burning through your valuable tuition credits to offset taxes that the Dividend Tax Credit would have otherwise covered.

The Solution

If you still have substantial tuition credits, it is almost always more tax-efficient to pay yourself a salary or bonus rather than a dividend. Salary income does not generate a Dividend Tax Credit, meaning your tuition credits are efficiently utilized to offset highly-taxed employment income without wasting any other credits.

Optimize Your Corporate Remuneration

Choosing between a salary, dividends, or a strategic mix of both requires a deep understanding of corporate tax integration, your personal spending needs, and your long-term retirement goals.

Don’t leave your tax strategy to chance—or risk wasting your hard-earned tuition credits. Contact the corporate tax specialists at Capstone LLP today to ensure your compensation strategy is perfectly aligned with your goals.